DeFi News

UMA enables DeFi developers to build synthetic assets

UMA is an open source protocol that allows two counterparties to create their own financial contracts and synthetic assets, backed by economic incentives that make them self-enforcing. UMA, short for Universal Market Access, is a decentralized platform for financial contracts that aims to allow precisely what the name suggests: universal market access.

The project has experienced steady traction in recent times and the expectation of new collaborations to improve the protocol is fostering good expectations for 2021.

Why UMA

Financial contracts and derivatives represent the core of the existing financial system. The emergence of the DeFi world and the development of a financial system that wants to become more ethical and open, thanks to permissionless systems such as blockchain, does not exclude the importance of derivatives and synthetic assets in its adoption.

In traditional finance, derivatives and other financial contracts are generally applied through two mechanisms.

- margining, in which counterparties post value guarantees as the contract varies

- legal recourse, in which a counterparty can sue the other party if the contract is not fulfilled.

Legal recourse is often limited to those who are larger and more powerful, limiting access and use of this tool, moreover in traditional systems moving money and margining a contract takes time.

The blockchain allows financial contracts to be margined continuously and on a near-real basis, thus enabling contracts with no legal recourse, no trust and entirely secured by economic incentives.

With significant advantages:

- elimination of barriers that limit access to financial markets;

- users in countries with weak financial structures could bypass local infrastructure limitations;

- universally programmable risk, smart contracts open up financial markets of all types, opening up great opportunities for decentralized financial products.

A truly global financial market.

How does UMA work

UMA consists of a decentralized, open source infrastructure for self-enforcing financial contracts on Ethereum.

Specifically, it consists of two elements

- Self-enforcing financial contract templates;

- Data Verification Mechanism (DVM), i.e. a “demonstrably honest” oracle used to evaluate and marginalize such contracts.

Combined, these two technologies enable the creation of synthetic, fast and secure derivatives on the Ethereum blockchain.

UMA financial contracts are contracts that do not require an on-chain price feed to function, thus reducing the use of oracles through incentives that tend to make counterparties commit to securing their positions without requiring any off-chain price feeds.

The incentive mechanism specifically allows counterparties to be rewarded for identifying inadequately secured positions, if a position is not liquidated it is assumed to be solvent (adequately secured).

Oracles are only used when liquidation is disputed.

UMA thus defines an open source protocol for creating and verifying financial contracts without trust, allowing anyone, anywhere, to design and create universally accepted financial contracts on Ethereum.

UMA Oracle

The Data Verification Mechanism (DVM) is the name given to the service performed by the UMA oracle. It does not provide on-chain price feeds, but is used exclusively to resolve settlement disputes and to resolve synthetic token contracts on expiry.

In the event of a dispute, a price request is sent to the DVM which proposes a vote among the UMA token holders in order to price the asset at a specific timestamp. The pricing is done via off-chain price feeds recorded via UMA’s Voter dApp service.

The DVM will aggregate the votes of the token holders and determine the final price of the asset at a given timestamp. The premise on which the DVM service is based is that any oracle on a public blockchain can be corrupted. For this reason, UMA is based on a system of economic incentives, so that any attempt at corruption is not profitable.

The goal is to build a mechanism whereby the Cost of Corrupting (CoC) is always greater than the profit that would be made from corrupting the Profit from Corruption (PfC) system, a formula where CoC>PfC, thus allowing for a “demonstrably honest” oracle.

This process takes place in three steps:

- Measuring the Cost of Corruption (CoC)

- Measuring Profit from Corruption (PfC)

- Maintaining CoC>PfC

If you want to learn more about these three processes, please refer to the UMA whitepaper.

UMA Synthetic Tokens

With UMA it is possible to launch synthetic assets that reference an underlying benchmark index, rather than relying on on-chain data via price oracles.

A trustless tokenization system that uses contracts to create ERC-20 tokens for synthetic cryptocurrency or real-world asset exposure.

UMA allows users to tokenize the price of anything in an open and decentralized way, global investors can get exposure to any existing asset or better use creativity to tokenize assets not yet conceived in traditional finance.

Governance tokens

At the heart of the protocol is the native UMA token, holders are empowered to contribute to important decisions, whether it be protocol parameters, types of assets supported, or whether to intervene in disputes over price requests, through the UMA protocol’s data verification mechanism.

The UK’s tax authority, Majesty’s Revenue and Customs (HMRC), released an update to its guidance on Wednesday, reported Bloomberg.

The new policy provides a series of “guiding principles” that act as general guidance in determining whether DeFi-related return or participation should be classified as income or capital gain.

How loan returns or staking is taxed depends on whether it is considered capital or income, however determining this can be a complex task. In the post, the HMRC admitted about this difficulty:

Token lending/staking via Decentralized Finance (DeFi) is a constantly evolving area, so it is not possible to establish all the circumstances in which a lender/liquidity provider makes a return on their activities and the nature of that performance. Instead, some guiding principles are established.

New policy to tax DeFi and staking

The latest guide sets out four distinct points designed to make it easier for people to determine the nature of their tax. Firstly, if the return received by the lender or liquidity provider is known “at the time the agreement is made”. If known, it would indicate a revenue receipt, but if unknown, it would indicate a capital receipt.

Second, if the return is realized through the disposal of a capital asset, it qualifies as capital. Conversely, if the borrower, or the DeFi lending platform, pays the yield to the lender/liquidity provider, the yield should be classified as income.

Third, the regulator indicated that lump-sum payments are “more likely” to qualify as principal; while recurring payments are “more likely” to be in the nature of revenue. Finally, the HMRC mentions the loan period as another variable that determines the nature of the repayment, everything will depend on whether it is “fixed or indefinite, short or long term”, he said.

The document presents some examples of how users can determine the nature of their loan return or participation. For example, if the return amount has already been agreed upon, say 5% per annum, it will most likely be a revenue receipt, the regulator said. On the other hand, if the income is “unknown and speculative”, it is probably a capital receipt.

As CoinDesk noted, the new policy is an update to previous guidance that had been published by HMRC in March 2021. According to that document, taxation of staking trades depended on whether the activity amounted to “taxable trading.” The wording closely resembled the established rules for taxing cryptocurrency mining, the outlet adds.

The US Securities and Exchange Commission (SEC) is interested in the fact that the definition of a stock market would now be much broader, also encompassing systems that allow buyers and sellers to communicate their interest in trading this type of asset, which which would include decentralized exchanges (DEX) such as Uniswap, PancakeSwap and many others for bringing together this type of people interested in trading digital currencies.

The measure would require platforms that meet these characteristics to register with the US Securities and Exchange Commission as securities brokers, and since decentralized exchanges would not be able to meet the demands required by this type of license, this could imply the imminent cessation of its operations throughout the United States.

More delicate than it seems

Some analysts and enthusiasts express concern about the possible repercussions this could have for the sectors associated with digital currencies.

In this regard, the DeFi sector enthusiast, Gabriel Shapiro, presented an even more delicate panorama for this type of exchange, since such a definition could also address even block explorers, such as Etherscan, precisely because they allow users to users interact with smart contracts to communicate business interests.

In this sense, it highlights that all this can be interpreted as a restriction on freedom of expression, for which it would be completely unconstitutional.

From a regulatory point of view, the SEC commissioner, Hester Peirce, also expressed her concerns and echoed some aspects mentioned above, placing special emphasis on the broad and diffuse nature of the changes proposed by the entity, which even go far beyond the scope and jurisdiction of the regulatory body.

On the other hand, Peirce criticized the fact that the interested community has very little time to read, understand and consider the proposal, which is not consistent with the implications it could have, since it would be making changes to an ecosystem that moves thousands of million dollars, which it could harm in unforeseen ways.

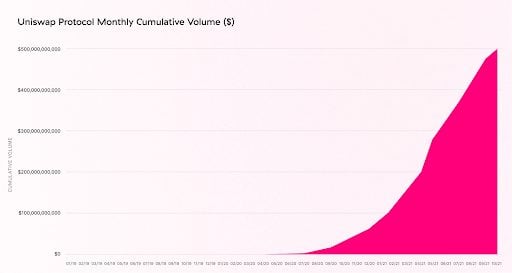

One of the best-known decentralized exchanges in the cryptocurrency market has just passed the US$500 billion transacted mark.

“We’re proud of the magnitude of this number, but we’re even happier knowing that millions of users have had direct access to markets they could trust were operating in their best interest.” – stated Uniswap Labs on Twitter.

About 2 billion of this volume was thanks to two scalability solutions integrated into the project:

“⚡️ $2 billion of this volume was contributed by @arbitrum and @optimismPBC deployments, which are starting to see significant traction!” – said Uniswap Labs.

Uniswap was created in November 2018, but it was conceived in 2016 by Vitalik Buterin (creator of Ethereum). With support from the Ethereum Foundation, programmer Hayden Adams made the idea come true.

Since then, the broker has not stopped growing and its UNI token is already worth 14.35 billion dollars.

With Uniswap, anyone can be an arbitrator between tokens using the blockchain, which narrows the price gap in small markets and gives incentives to balance asset prices using blockchain and centralized brokerages.

Currently, UNI is traded in several brokers in EEUU and around the world, such as Coinbase, Bitfinex and Binance US.

“We are so grateful to be together on this journey with our incredible community, and we can’t wait to hit the $1tn mark.”

Shiba Inu: Celebration for the Burning of 176 Million SHIB in a Historic Transaction

Nomura Group Unveils Bitcoin Fund Catering to Institutional Investors

Bitcoin Surges to $32,500 in China: Here’s Why

US National Debt Reaches a Record of $33 Trillion: Economic Crisis in Perspective

This Analyst Predicts a Bright Bullish Future for Chainlink (LINK)

FTX Files Lawsuit Against Sam Bankman-Fried’s Parents in Effort to Recover Funds

Crypto Enforcement Funds Under Scrutiny: Congressman Emmer Calls For Restrictions On SEC

These 3 AI Crypto Coins are Bullish in 2023 – Render, Fetch.ai, yPredict

-

Opinion2 years ago

Opinion2 years agoXRP: FOX Business Senior Correspondent Says SEC Is Losing Its Lawsuit Against Ripple

-

Tutorials3 years ago

Tutorials3 years agoHow to Earn, Farm and Stake CAKE on PancakeSwap with Trust Wallet

-

Altcoins News3 years ago

Projects with ongoing migration from Ethereum to Cardano

-

NFT3 years ago

CardanoKidz: The first NFTs arrive at Cardano

-

Tutorials3 years ago

How to set up a Bitcoin node: beginner’s guide

-

NFT3 years ago

SpaceBudz: new astronaut NFTs on Cardano

-

DeFi News3 years ago

Uniswap vs PancakeSwap: Full analysis

-

DeFi News3 years ago

Liqwid Finance the first DeFi project on Cardano: everything you need to know