DeFi News

Uniswap vs PancakeSwap: Full analysis

Ethereum’s unstoppable ride since its December 2020 launch of the Beacon Chain was slowed for some in February 2021 — the troubles, ironically, came from its price rise. The world’s second-biggest cryptocurrency, pushed by a new all-time-high (ATH) of over $2,000 and a surge in the popularity of staking apps, began to stutter due to congestion and outrageous gas fees, sometimes in excess of $50 a transaction, causing some users and developers to jump ship to other alternatives.

The Binance Smart Chain (BSC) and its under-the-radar exchange PancakeSwap cashed in on this migration in a big way, thus kicking off new inter-chain rivalries between Ethereum and BSC — and their respective flagship exchanges Uniswap and PancakeSwap — that may decide the foreseeable future of DeFi.

What is PancakeSwap?

PancakeSwap is a decentralized exchange (DEX) powered by the Binance Smart Chain (BSC), which uses an AMM (automated market maker) model to fulfill orders. As such, PancakeSwap replaces an order book with a liquidity pool.

Liquidity providers interact with the pool and receive LP tokens that represent their share in the pool. These tokens are key to removing their share from the pool. Since the platform runs on BSC, the tokens adhere to the platform’s BEP-20 token standards.

Furthermore, the LP tokens come in different “flavors” influenced by the token deposited in the pool.

What is Uniswap?

Uniswap is the most popular Ethereum-based DEX that uses an AMM model, employs liquidity pools instead of order books and has LP tokens for liquidity providers. Uniswap is the mother chain of PancakeSwap, which uses the original Ethereum blockchain to run its network as opposed to BSC. As one of the first wildly successful DeFi protocols, most DEXs have, in one way or another, borrowed features from Uniswap to run their own platforms.

Note that the AMM model removes the need to have a partner on the other side of a buy or sell order for a trade to go through. Consequently, less trading time is consumed on DEXs using this model. By removing the need to go through KYC (know-your-customer) procedures, these exchanges give access to decentralized token swapping to more people.

Why the rivalry between PancakeSwap and Uniswap?

After an incredible 2020 in which it rewrote the rules for decentralized exchanges, Uniswap has been viewed as a benchmark for DEXs, considering that most DeFi-focused projects are trying to take up the mantle in becoming the leading platform for token swaps.

PancakeSwap is the unofficial winner to this war, with its liquidity increasing by over 1,000% in approximately two months. Furthermore, PancakeSwap’s volume had skyrocketed from a meager $37 million to a “whopping” $1 billion within the first 49 days of 2021.

Interestingly, its growth has been attributed to the shortcomings of the Ethereum blockchain that hosts Uniswap. The ETH-powered network suffers from scalability issues due to its reliance on the proof-of-work (PoW) consensus mechanism. As a result, the congestion on the platform causes a rise in transaction costs or gas.

In December 2020, Ethereum started the migration from a PoW to a PoS (proof-of-stake) consensus mechanism through the launch of Ethereum 2.0, which is expected to solve the scalability issue. Unfortunately, the complete rollout is expected to take approximately two years.

Why Binance Smart Chain?

Binance Smart Chain continues to gain more foothold in the DeFi space. Some of the key areas BSC succeeds at include:

Efficiency and affordability

Instead of a PoW system, it uses a version of PoS called proof-of-staked-authority (PoSA). This version provides a three-second block time, which means that transactions settle faster and fees are substantially lower since there is no network congestion.

Inter-Blockchain compatibility

BSC is compatible with other decentralized platforms. For example, BSC is compatible with Ethereum because it supports the Ethereum Virtual Machine (EVM). This means that Ethereum developers can quickly transfer (port) their projects to Binance by turning a few nobs, so to speak.

PancakeSwap flippens Uniswap, Uniswap overtakes Coinbase

In February 2021, PancakeSwap had briefly usurped Uniswap as the largest AMM-based exchange. The daily trading volume on the BSC-powered project DEX was over $400 million more than the ETH-based platform on February 19.

Notably, the rise had been steady, recording over $1 billion in volume per day. Ethereum recorded $16 million in gas fees in a single day, while BSC users only had to pay a tiny fraction of that sum.

However, as of March, Uniswap had regained its place above PancakeSwap — but a new player, MDEX, has already taken the number one spot above Uniswap, showing just how fast the decentralized trading world moves.

Uniswap had already exceeded the trading volume of Coinbase, the largest centralized cryptocurrency exchange. On the other side, apart from an increasing volume on PancakeSwap, the exchange’s CAKE token had also recorded significant growth, gaining over 6,000% in less than six months.

PancakeSwap vs Uniswap: Top DEXs compared

Native tokens

CAKE is PancakeSwap’s base asset, which doubles as a governance token, as well as provides farming and staking functionalities. Users can get their hands on CAKE by either providing liquidity, staking or buying them on an exchange (the staking option allows holders to earn more tokens).

Note that CAKE tokens issued to liquidity providers are tradable on the open crypto market, just like standard coins.

On the other hand, we have UNI tokens, Uniswap’s native asset, which its developers had airdropped to initial users of its platform back in September 2020. However, the token’s real use case on the platform, apart from governance, is yet to be defined.

As such, by the time UNI’s use case is more clarified, if it ever is, CAKE is expected to have gained more traction. For other governance purposes, PancakeSwap has another token called SYRUP, which allows holders to receive 40% of CAKE emissions — Syrup is not designed to be sold, since it is needed to unstake any staked CAKE.

Adoption

It’s hard to quantify the two top DEXs on this one. While PancakeSwap’s adoption rate is on the rise, Uniswap is older and has a considerable user base. It’s among the few projects that fished DeFi from the shadows by introducing AMM functionalities that no other project had successfully executed before.

However, PancakeSwap seems to be on its way to pass Uniswap, owing to the rise in adoption of both the Binance Smart Chain and the CAKE token. As is common in the crypto space, the price of a digital asset responds to adoption or at least demand.

As of now, there appears to be more demand for CAKE than UNI. Therefore, the price rise is a sign that more people are leaning towards the Uniswap clone.

Transaction costs

Ethereum clearly lost the battle on transaction costs at the moment, leaving the door wide open for more efficient platforms with smart contract capability. With Uniswap running on the second-largest blockchain, gas fees have been exponentially rising.

The problem is even bigger for Uniswap users who can only trade small amounts, as the gas costs would eat into their profits. By using a scalable network like BSC, PancakeSwap is able to offer dramatically lower transaction costs.

On BSC, transaction costs are in terms of pennies compared to Ethereum, whose fees can go up to a few hundred dollars. Apart from saving users from high gas fees, BSC also facilitates faster transactions.

Number of listed tokens

Uniswap has the edge here, since it has over 1,500 tokens compared to PancakeSwap’s 200+ listed tokens, mainly because Uniswap has been around much longer and caters to Ethereum users. However, in September 2020, the speed and sheer number of tokens listed on the network raised eyebrows as Uniswap reported an average of 150 token pairs added a day for a whole seven days — while an open system drives freedom, this freedom also extends to malicious actors. As a result of Uniswap’s permissionless system, fake projects had surged, eager to cash in on hasty investors. For example, Uniswap saw the listing of “Uniswap Exchange Token,” which had no relation at all to Uniswap besides being listed on the platform.

PancakeSwap boasts the listing of successful and unique tokens like FRONT and BAKE — but the same “low-quality listing” issue that plagues Uniswap is also existent in the BSC-based fork.

Liquidity and trading volume

Although the liquidity on PancakeSwap is on the rise, Uniswap is still leading. Most tokens on Uniswap have substantial liquidity compared to those on PancakeSwap. More liquidity providers prefer Uniswap since PancakeSwap’s liquidity provision incentives favor those that deposit exotic tokens that are the most volatile.

On the other hand, PancakeSwap has already surpassed Uniswap’s one-day trading volume. However, due to the DeFi ecosystem’s volatility, the BSC-powered platform needs to maintain an upward trajectory to permanently beat Uniswap on trading volume.

Security and community

Although PancakeSwap and Uniswap are both decentralized, PancakeSwap benefits from the Binance ecosystem’s support. However, Uniswap also has a large community, thanks to its early entrance into the DeFi scene.

PancakeSwap is attempting to bridge the gap in users created by their relatively recent arrival on the DeFi scene by attracting a loyal following via lotteries, competitions and other similar incentives.

What’s next for Binance Smart Chain?

Again, it needs to be said that the PancakeSwap-Uniswap rivalry goes beyond the DEXs themselves, since it also illustrates the key differences between the Ethereum blockchain and Binance Smart Chain.

BSC currently seems to be on the gaining side, with its liquidity growing exponentially. Binance’s native token, BNB, is reaping the rewards from the DeFi boom, occupying a seat on the top five leading cryptocurrencies in market cap on CMC.

Notably, the high volumes on BSC indicate the need for cheaper and faster transactions. Ethereum’s high gas costs seem to be the highest contributor to users’ departures toward BSC-based DeFi networks. For instance, between January and February 2021, BSC recorded an increase in unique users from 12,700 to over 50,000.

Since users came with an increase in trading volume, on Feb. 9, 2021, BSC’s trading volume reached $6.84 billion, while that of the second-largest blockchain stood at $5.42 billion. Furthermore, BSC is seeing a rise in new decentralized applications (DApps) like BakerySwap, JulSwap, Autofarm and many more platforms.

The increased competition will put immense pressure on Ethereum developers to speed up, or at least stick to, the deadlines that mark the roadmap leading to its proof-of-stake final form which should put an end to its current scaling issues.

The UK’s tax authority, Majesty’s Revenue and Customs (HMRC), released an update to its guidance on Wednesday, reported Bloomberg.

The new policy provides a series of “guiding principles” that act as general guidance in determining whether DeFi-related return or participation should be classified as income or capital gain.

How loan returns or staking is taxed depends on whether it is considered capital or income, however determining this can be a complex task. In the post, the HMRC admitted about this difficulty:

Token lending/staking via Decentralized Finance (DeFi) is a constantly evolving area, so it is not possible to establish all the circumstances in which a lender/liquidity provider makes a return on their activities and the nature of that performance. Instead, some guiding principles are established.

New policy to tax DeFi and staking

The latest guide sets out four distinct points designed to make it easier for people to determine the nature of their tax. Firstly, if the return received by the lender or liquidity provider is known “at the time the agreement is made”. If known, it would indicate a revenue receipt, but if unknown, it would indicate a capital receipt.

Second, if the return is realized through the disposal of a capital asset, it qualifies as capital. Conversely, if the borrower, or the DeFi lending platform, pays the yield to the lender/liquidity provider, the yield should be classified as income.

Third, the regulator indicated that lump-sum payments are “more likely” to qualify as principal; while recurring payments are “more likely” to be in the nature of revenue. Finally, the HMRC mentions the loan period as another variable that determines the nature of the repayment, everything will depend on whether it is “fixed or indefinite, short or long term”, he said.

The document presents some examples of how users can determine the nature of their loan return or participation. For example, if the return amount has already been agreed upon, say 5% per annum, it will most likely be a revenue receipt, the regulator said. On the other hand, if the income is “unknown and speculative”, it is probably a capital receipt.

As CoinDesk noted, the new policy is an update to previous guidance that had been published by HMRC in March 2021. According to that document, taxation of staking trades depended on whether the activity amounted to “taxable trading.” The wording closely resembled the established rules for taxing cryptocurrency mining, the outlet adds.

The US Securities and Exchange Commission (SEC) is interested in the fact that the definition of a stock market would now be much broader, also encompassing systems that allow buyers and sellers to communicate their interest in trading this type of asset, which which would include decentralized exchanges (DEX) such as Uniswap, PancakeSwap and many others for bringing together this type of people interested in trading digital currencies.

The measure would require platforms that meet these characteristics to register with the US Securities and Exchange Commission as securities brokers, and since decentralized exchanges would not be able to meet the demands required by this type of license, this could imply the imminent cessation of its operations throughout the United States.

More delicate than it seems

Some analysts and enthusiasts express concern about the possible repercussions this could have for the sectors associated with digital currencies.

In this regard, the DeFi sector enthusiast, Gabriel Shapiro, presented an even more delicate panorama for this type of exchange, since such a definition could also address even block explorers, such as Etherscan, precisely because they allow users to users interact with smart contracts to communicate business interests.

In this sense, it highlights that all this can be interpreted as a restriction on freedom of expression, for which it would be completely unconstitutional.

From a regulatory point of view, the SEC commissioner, Hester Peirce, also expressed her concerns and echoed some aspects mentioned above, placing special emphasis on the broad and diffuse nature of the changes proposed by the entity, which even go far beyond the scope and jurisdiction of the regulatory body.

On the other hand, Peirce criticized the fact that the interested community has very little time to read, understand and consider the proposal, which is not consistent with the implications it could have, since it would be making changes to an ecosystem that moves thousands of million dollars, which it could harm in unforeseen ways.

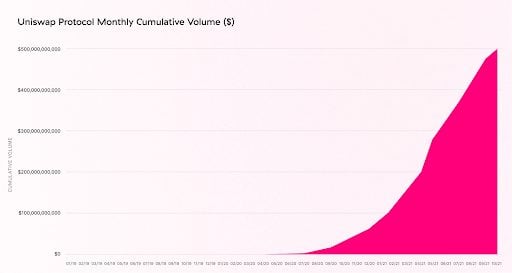

One of the best-known decentralized exchanges in the cryptocurrency market has just passed the US$500 billion transacted mark.

“We’re proud of the magnitude of this number, but we’re even happier knowing that millions of users have had direct access to markets they could trust were operating in their best interest.” – stated Uniswap Labs on Twitter.

About 2 billion of this volume was thanks to two scalability solutions integrated into the project:

“⚡️ $2 billion of this volume was contributed by @arbitrum and @optimismPBC deployments, which are starting to see significant traction!” – said Uniswap Labs.

Uniswap was created in November 2018, but it was conceived in 2016 by Vitalik Buterin (creator of Ethereum). With support from the Ethereum Foundation, programmer Hayden Adams made the idea come true.

Since then, the broker has not stopped growing and its UNI token is already worth 14.35 billion dollars.

With Uniswap, anyone can be an arbitrator between tokens using the blockchain, which narrows the price gap in small markets and gives incentives to balance asset prices using blockchain and centralized brokerages.

Currently, UNI is traded in several brokers in EEUU and around the world, such as Coinbase, Bitfinex and Binance US.

“We are so grateful to be together on this journey with our incredible community, and we can’t wait to hit the $1tn mark.”

Shiba Inu: Celebration for the Burning of 176 Million SHIB in a Historic Transaction

Nomura Group Unveils Bitcoin Fund Catering to Institutional Investors

Bitcoin Surges to $32,500 in China: Here’s Why

US National Debt Reaches a Record of $33 Trillion: Economic Crisis in Perspective

This Analyst Predicts a Bright Bullish Future for Chainlink (LINK)

FTX Files Lawsuit Against Sam Bankman-Fried’s Parents in Effort to Recover Funds

Crypto Enforcement Funds Under Scrutiny: Congressman Emmer Calls For Restrictions On SEC

These 3 AI Crypto Coins are Bullish in 2023 – Render, Fetch.ai, yPredict

-

Opinion2 years ago

Opinion2 years agoXRP: FOX Business Senior Correspondent Says SEC Is Losing Its Lawsuit Against Ripple

-

Tutorials3 years ago

Tutorials3 years agoHow to Earn, Farm and Stake CAKE on PancakeSwap with Trust Wallet

-

Altcoins News3 years ago

Projects with ongoing migration from Ethereum to Cardano

-

NFT3 years ago

CardanoKidz: The first NFTs arrive at Cardano

-

Tutorials3 years ago

How to set up a Bitcoin node: beginner’s guide

-

NFT3 years ago

SpaceBudz: new astronaut NFTs on Cardano

-

DeFi News3 years ago

Liqwid Finance the first DeFi project on Cardano: everything you need to know

-

DeFi News3 years ago

PancakeSwap has surpassed Ethereum in transaction volume